Today after the end of the session on Wall Street, traders will be offered first the results for the 1st quarter of 2024 from those American technology companies. Alphabet ( GOOGL.US ), Microsoft ( MSFT.US ) and Intel ( INTC.US ). At first, these companies could help strengthen sentiment in the US technology sector. However, traders should keep in mind that the markets are unpredictable and a nice profit does not necessarily mean an increase in share prices after the announcement – disappointed by the results of the Tesla company sent the shares of the electric car manufacturer into the air, while the company Meta Platforms fell in the pre-trading phase, although it performed better oekvan consequences. Let’s take a quick look at what the market is like from Alphabet, Microsoft and Intel and what to avoid.

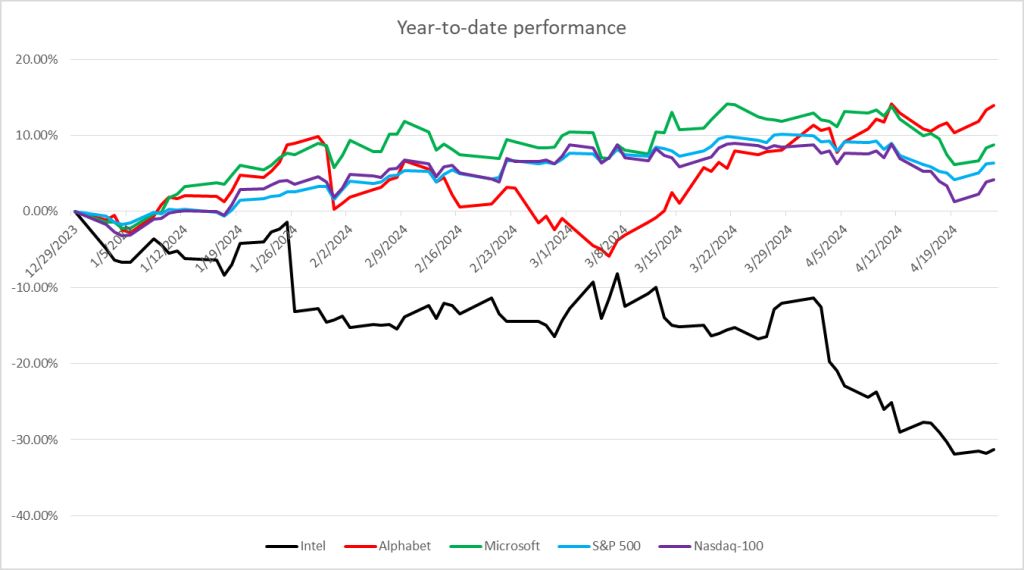

While the companies Alphabet and Microsoft have improved the performance of the market this year, Intel will be significantly worse. Source: Bloomberg Finance LP, XTB Research

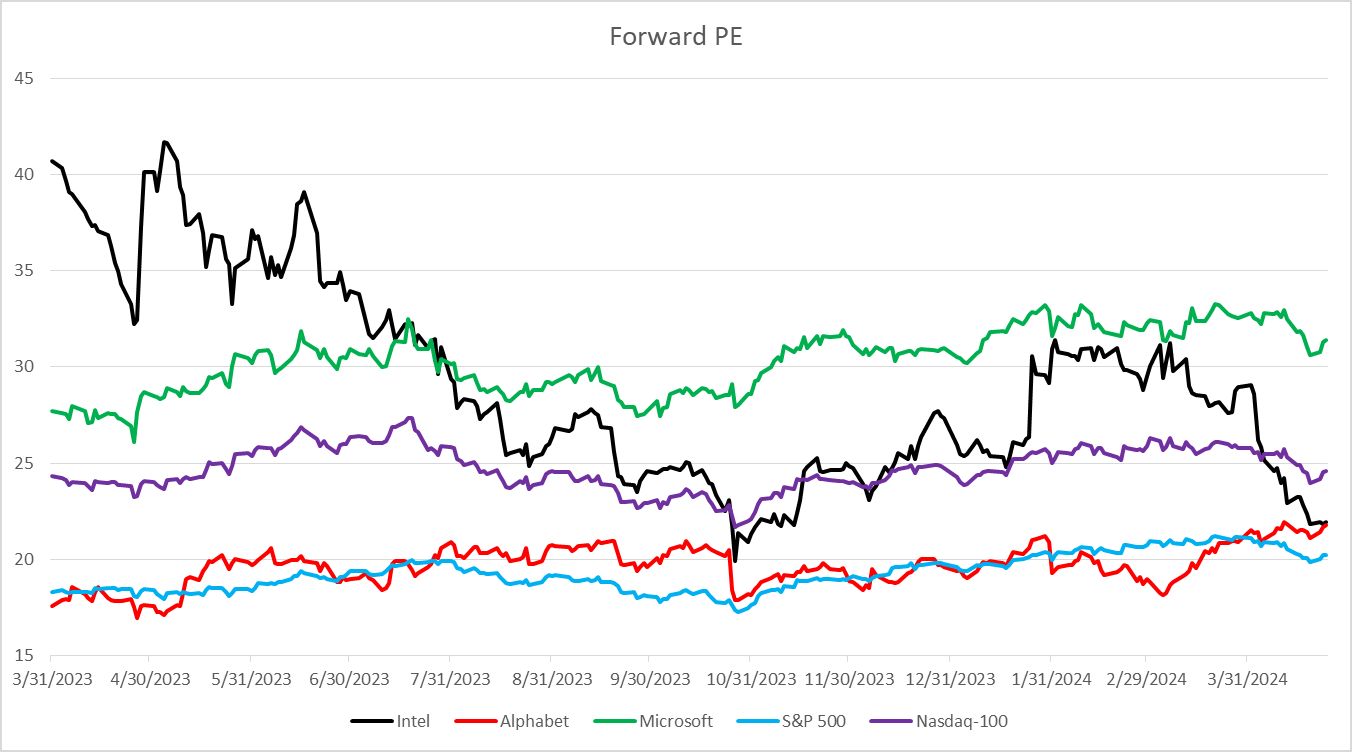

Of the major US technology companies reporting earnings today, Microsoft appears to be the most expensive in terms of forward P/E ratio. Source: Bloomberg Finance LP, XTB

Alphabet

Alphabet (GOOGL.US) has outperformed the S&P 500 and Nasdaq-100 this year and has gained 14% since the beginning of the year. At first, Alphabet’s focus will be on the next thing – artificial intelligence, the cloud and advertising. Open markets indicated a 5.7% move in the share price after the results were announced.

Alphabet is expected to see no more than 13% intercompany growth in total demand for 1Q 2024. Cloud growth is expected to remain strong. If the growth of this segment has slowed down as its size has increased, analysts expect that the cross-sectional growth of cloud needs will remain relatively the same as in the 4th quarter of 2023, which is the growth not the growth recorded in the 3rd quarter of 2024.

The cloud will be closely watched because it is Alphabet’s fastest-growing segment, but investors will also pay attention to advertising – the company’s biggest source of revenue. The company is expected to post more than 10% growth in ad revenue, which represents an acceleration from the 9.5% reported in Q4 2023. If confirmed, this will mark the fifth consecutive quarter of accelerating ad revenue growth.

Last but not least, the comments on artificial intelligence will be carefully monitored. Investing in AI will help drive Google Cloud’s growth, so the two areas of analytics are likely to be combined.

Estimated for Q1 2024

- Revenue: $79.04 billion (Meziron +13.3%)

- Google Services: $69.06 billion (Meziron +11.5%)

- Google Advertising: $60.18 billion (Meziron +10.3%)

- Google Cloud: $9.37 billion (+25.8% YoY)

- Other: $372M (+29.3% YoY)

- Captured: USD 96 million (+14.4% YoY)

- Revenues excluding operating expenses: $66.07 billion (+13.8%)

- Gross profit: $44.72 billion (+14.1%)

- Gross margin: 56.9% versus 56.1% a year ago

- Operating income: USD 22.39 billion (+28.6% YoY)

- Google Services: $24.3 billion (+11.8% YoY)

- Google Cloud: $672 million (+252% meziron)

- Other: -$1.12 billion

- Captured: -$1.65 billion

- Operating margin: 28.6% versus 25% a year ago

- sure revenue: USD 19.6 billion (+30.2% yoy)

- ist mare: 22.4% versus 21.6% a year ago

- Adjusted earnings per share: $1.53 versus $1.17 a year ago

- Capital revenues: USD 10.24 billion (+62.8% y-o-y)

Alphabet (GOOGL.US) is near all-time highs. In the first half of April 2024, the shares fell, but since then they have managed to recover all their losses. The stock is trading just below the resistance at USD 160, and strong first quarter results should push the price to a new record level. Source: xStation5

Microsoft

Microsoft (MSFT.US) has outperformed the S&P 500 and Nasdaq-100 this year. Since the beginning of the year, it has rallied no more than 8%, thus continuing a 90% rally in 2023. As for the upcoming economic results, investments will be made in the cloud business, which has recently been the key engine of growth. Open markets expect a 4.8% move in the share price after the results are announced.

It is expected that the company Microsoft will grow in the current fiscal quarter of 2024 (calendar 1st quarter of 2024) no more than 15% of interannual growth of total needs. It is expected that the cloud will remain the largest segment in terms of needs and the main engine of growth. Growth in the intelligent cloud segment is expected to slow to 19% year-on-year from 20.3% year-on-year in fiscal Q2 2024 (calendar Q4 2023). It is expected, however, that it will be faster than the 15.9% average growth recorded in the same period a year ago. In the ir category of income from the cloud – income from the commercial cloud – however, for the first time in the history of the economy, growth has slowed to below 20% between years.

Due to the darkness, the result will be artificial intelligence. The songs are how to influence the growth in the Azure cloud. In fiscal 1st quarter 2024 (calendar 3rd quarter 2023), AI contributed 300 basis points to Azure growth, and in fiscal 2nd quarter 2024 (calendar 4th quarter 2023), this contribution increased to 600 basis points.

The fiscal 3rd quarter of 2024 was thus the first full quarter after the consolidation of Activision into Microsoft after the acquisition. He said the acquisition helped accelerate demand growth, but it was also a drag on profits.

Around the 3rd fiscal quarter of 2024

- Revenue: $60.88 billion (+15.2% y-o-y)

- Productivity and Business Processes: $19.54 billion (Meziron +11.6%)

- Intelligent Cloud: $26.25 billion (+18.9% YoY)

- More personal income: USD 15.07 billion (+13.6% y/y)

- Commercial cloud revenue: $33.93 billion (Meziron +19%)

- Gross profit: $42.31 billion (+15.2%)

- Gross mare: 69.1% versus 69.5% a year ago

- Operating income: USD 25.64 billion (+14.7%)

- Productivity and Business Processes: $9.93 billion (Meziron +15%)

- Intelligent Cloud: $11.71 billion (+23.6% YoY)

- More personal income: USD 4.51 billion (+6.6% y-o-y)

- Operating margin: 43.0% versus 42.3% a year ago

- sure income: USD 21.06 billion (+15.1%)

- ist mare: 34.0% versus 34.6% a year ago

- Adjusted earnings per share: $2.83 versus $2.45 a year ago

Microsoft (MSFT.US) reached new all-time highs above $430 per share in the 2024 quarter. Later, however, the shares began to encounter problems and fell by about 8% from their record highs. The decline was stopped at the support zone moving below the USD 400 mark and the shares started to recover. Will this fiscal quarter’s earnings provide fuel for a rally to new all-time highs? Source: xStation5

Intel

Although Intel (INTC.US) is a smaller company and may not attract as much attention as Alphabet or Microsoft, it will also be closely watched at first. After all, this is one of the best American semiconductor events. This year, however, Intel has significantly underperformed the S&P 500 and Nasdaq-100 indexes, when it has fallen by about 30% since the beginning of the year. Open markets indicated a 7.4% movement in the share price after the results were announced.

It is expected that Intel will see an 8.5% increase in total demand in the first quarter of the year, while the Client Computing segment should see a 30% increase and the Datacenter & AI segment should see a 20% drop in demand. A lot of attention will be paid to Intel Foundry again. Intel is trying to become a global company dealing with the famous ip. Foundry business is IP manufacturing for the third party, just like TSMC. Intel received many funds from the Chips Act for various production capacities, but growth is limited by chips. One of the biggest things that separates it from TSMC is the fact that Intel also designs its own chips, and this limits the growth potential of its Foundry business. For? Some companies, such as AMD, may not want to use the Intel Foundry service because they would have to submit their new designs to Intel, their main competitor. Intel, however, should file orders between companies that do not design IPs similar to those used by Intel. Among the top five are, for example, Nvidia and Apple.

Given that Intel identifies services as another growth engine, the prospects of this segment will be closely watched. However, it is important to remember that this segment makes up less than 2% of Intel’s total revenue and its growth has slowed down in the second half of 2023, so it will take some time before it becomes really significant for the company.

Estimated for Q1 2024

- Revenue: $12.71 billion (+8.5% y-o-y)

- Client Computing: $7.39 billion (+28.1% YoY)

- Datacenter & AI: $3.45 billion (-19.2% meziron)

- Network & Edge: $1.35 billion (-13.8% YOY)

- Intel Foundry: $170 million (+44% meziron)

- Mobile Eye: $372M (-18.8% YoY)

- Gross profit: USD 5.70 billion (+24.8% mezron)

- Gross mare: 44.5% vs. 38.4%

- Operating income: 562 million USD (-294 million USD y/y)

- Operating margin: 4.8% versus -2.5% a year ago

- sure revenue: $580 million (-$169 million prior year)

- ist mare: 4.5% versus -1.5% a year ago

The company Intel (INTC.US) will make a significant investment this year. Shares continued to move higher, breaking through a series of support lines and hitting their highest level in over a year. In the second half of April, however, the sale was stopped, and I was positively surprised at first about the results for the 1st quarter to help start the upward correction. Source: xStation5

X-Trade Brokers

X-Trade Brokers (XTB) is an international brokerage house that provides professional conditions for trading CFDs on forex, indices, commodities, cryptocurrencies and for investing in shares and ETFs. He is constantly improving his services, which is evidenced by a number of international awards, and this is also confirmed by the domestic award of Broker of the Year and Forex Broker of the Year, which was repeated at the MoneyExpo Investment Summit. For its clients, XTB offers professional trading platforms MetaTrader 4 and xStation 5 with an integrated calculator, free extension, 24-hour customer support, free extension and daily news from the financial markets.

The distribution of contracts are complex instruments and due to the use of financial leverage, they are associated with a high risk of rapid financial loss. In the case of 72% of the retail investors, the trading with installment contracts with this provider resulted in a loss. You should make sure you understand how the installment contract works and whether you can afford the high risk of losing your funds.

Tags: expect beginning big technologies today

-

{kind=link}